Introduction: A Cost Threshold Being Crossed

Digital transformation rarely occurs through grand declarations; it accumulates through incremental innovations until the industry looks back to find the landscape irrevocably changed. The 'The Digital Switch' forum at FESPA 2026 in Barcelona serves as the stage to examine this cumulative change [1]. Our research question is: For small-to-medium Taiwanese printing firms primarily using screen printing for garments and home textiles, has digital textile printing reached an inflection point warranting production capacity reallocation? If so, what are the criteria for this turning point, and how wide is the window of opportunity?

This question carries urgent practical relevance for the Taiwanese textile supply chain. Long esteemed for contract manufacturing and functional fabrics, the printing segment remains anchored in traditional screen printing logic, relying on high-volume runs to amortize plate-making and color-separation costs. However, as brand order structures shift from 'low-variety, high-volume' to 'high-variety, low-volume,' the premise of amortizing costs is fraying. This article argues that the key to determining the inflection point lies not in the technological novelty of the equipment itself, but in whether the cost curve intersection has fallen within the scale of mainstream orders [1]

The contributions of this article are threefold:

・First, it integrates the clues of equipment growth, ink compliance, and demand structure revealed at the FESPA 2026 forum into a testable 'inflection point criterion'

・Second, it maps these criteria into actionable decisions across three levels: Taiwanese SME printers, designers, and brand owners

・Third, it explicitly flags the evidentiary limitations of relying on a single exhibition source, avoiding the misreading of an industry event's optimistic narrative as settled market fact

Literature and Current Status Review: The Convergence of Three Forces and Gaps in Existing Discussions

This section defines three clusters of existing discourse and identifies where they remain unconverged. The FESPA 2026 forum, hosted by FESPA Textile Ambassador Debbie McKeegan, brought together perspectives from Gart Davis, Kerry Maguire King, Mitesh Patel of Premier Textiles, and Duncan Ferguson of Epson, spanning print-on-demand, fabric supply, garment decoration, design, and digital manufacturing technologies [1]. Their discussion can be synthesized into three intertwined main threads

The first thread is the shift in market structure. The forum's assessment of the post-pandemic industry landscape was candid: the reshoring wave that many based their product strategies on has effectively stalled, while geopolitical factors, tariffs, and energy costs have raised operational difficulties for traditional textile producers [1]. Against this backdrop, home decoration, fashion, and promotional gifting were identified as the segments most likely to drive recovery, with on-demand digital printing, design, and production accelerating once again [1]

The second thread is the shift of sustainability from a topic to a regulation. The forum noted that while sustainability briefly faded from headlines, it is a structural force returning with even stronger mandatory regulatory power, with digital product passports being one such concrete manifestation [1]. In other words, the disclosure of environmental footprints is no longer just a marketing option for brands; it is gradually becoming a traceable compliance requirement

The third thread is innovation in supply-side costs and materials. Facing energy costs and compliance pressures, fabric suppliers are opting for structural cost reductions without sacrificing specifications, for example, completing pretreatment at the mill level and shipping directly to the customer, saving a link in the chain to lower landed costs [1]. The forum simultaneously emphasized a refusal to cut costs by lowering GSM, altering thread counts, or swapping blends, as this erodes cross-platform output quality consistency and long-term supply trust [1]. On the sustainability front, take-back recycling services have emerged, involving crushing production waste (pre-consumer waste) to re-spin into fibers for re-weaving, alongside cases of printing on 100% recycled cotton [1]

These three threads hold up individually in existing discussions; the gap lies in the fact that they are rarely integrated into a decision-making criterion for 'when to transform.' Our analysis concludes that market structure (demand fragmentation), regulation (mandatory sustainability disclosure), and supply-side costs (material and pretreatment optimization) all point toward the same direction: redefining competitive advantage from 'scale' to 'flexibility and traceability.' This is the comprehensive perspective this article aims to provide

It is worth noting that, methodologically, one should maintain a critical distance from single exhibition sources. Research evaluating digital news and media sources indicates that the commercial motives and framing methods of sources affect information credibility, requiring cross-validation rather than blind acceptance [5][6]; market-oriented information production may also amplify signals favoring specific industry narratives [2]. As an industry exhibition, FESPA itself is a stakeholder in the equipment ecosystem; therefore, when citing its data, we position it as 'trend signals within the industry' rather than neutral market statistics

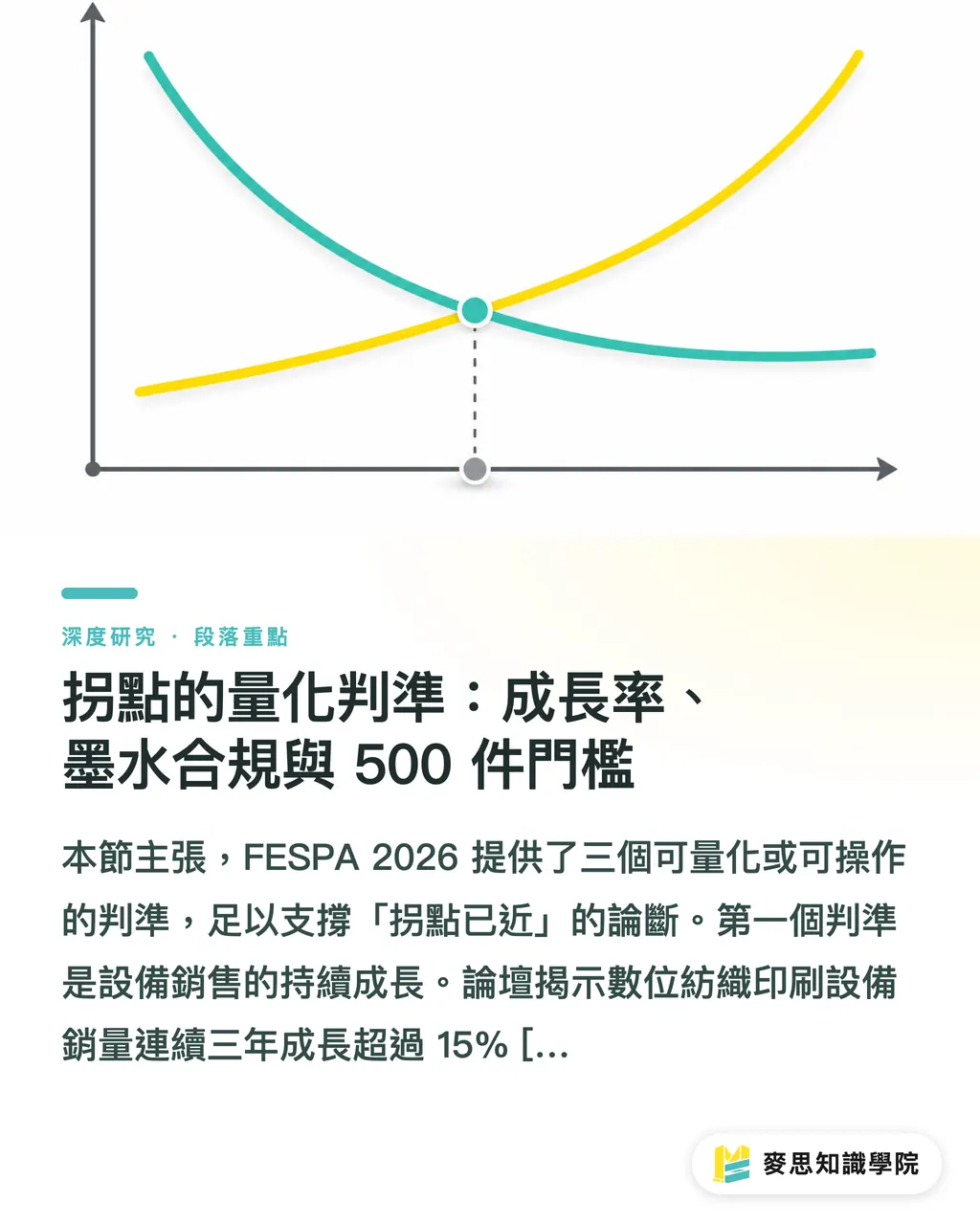

Quantitative Criteria for the Inflection Point: Growth Rates, Ink Compliance, and the 500-Unit Threshold

This section argues that FESPA 2026 provided three quantifiable or actionable criteria sufficient to support the assertion that an 'inflection point is near.' The first criterion is the sustained growth in equipment sales. The forum revealed that digital textile printing equipment sales have grown by over 15% for three consecutive years [1]. Our analysis posits that while high single-year growth might stem from a low base or one-off replacement cycles, double-digit growth sustained over three years is more likely to exclude short-term fluctuations, indicating structural rather than cyclical demand

The second criterion is the maturity of eco-friendly ink compliance. Water-based pigment inks can now pass most EU environmental certifications [1]. The significance of this lies not only in the environment but in removing two long-standing obstacles to digital printing: compliance thresholds and post-processing workflows. Compared to dye inks, pigment inks typically eliminate wet processes such as steaming and washing. Our analysis suggests that in an environment of elevated energy costs, this effectively compresses the unit variable cost of the digital route further, echoing the backdrop of energy pressure mentioned in the forum [1]

The third criterion is the most critical: the 500-unit cost intersection point. The forum explicitly stated that traditional screen printing has clearly lost its price advantage for runs under 500 units [1]. The cost structure of screen printing is dominated by fixed costs, plate-making and color separation, which must be amortized by volume; digital printing has almost no plate-making costs, but a higher unit variable cost. The intersection of these two cost curves determines which method prevails at a specific batch size. Our analysis posits that the 500-unit figure is significant because it falls within the mainstream order scale for fast fashion and promotional items, meaning the inflection point is not occurring in the niche proofing market, but is actively encroaching on the core revenue range of printing plants

Viewing these three criteria together, the driving force behind the trend stems from the demand side rather than purely technological push. The forum attributes this to the demand from fast-fashion brands for 'small-batch, multi-variety' orders [1]. As the print volume per design decreases and the number of styles increases, the frequency of screen changes and inventory risk climb simultaneously; the plate-less and print-on-demand nature of the digital route shifts from an 'alternative' to the 'default.' We thus infer that the essence of this inflection point is not that equipment is becoming cheaper, but that the order structure makes it impossible to amortize fixed costs

From Supply Chain to Creative Tempo: How Mechanisms are Being Rewritten

This section analyzes how the digital shift is rewriting operational mechanisms up and down the supply chain. Looking upstream, the 'mill-level pretreatment direct-to-customer' model in fabric supply [1] is complementary to digital printing demands. Digital pigment or dye printing is highly sensitive to the uniformity of fabric pretreatment; if pretreatment is standardized at the mill and shipped directly, printing plants can eliminate the equipment and labor for in-house sizing while achieving more stable output quality. Our analysis suggests this 'outsourcing of pretreatment' actually lowers the implicit barrier for SMEs to adopt digital equipment

Looking downstream, the digital route shortens the distance between proofing and mass production, consequently changing the creative tempo of designers. The forum pointed out that a shortened rapid proofing cycle changes the creative tempo, allowing designers to iterate through shorter feedback loops [1]. Under traditional screen printing, a change in colorway or pattern means re-making plates and costs, with design freedom constrained by the economics of the method; the digital route compresses the marginal cost of each modification to near zero, allowing creation to approach 'real-time trial and error.' Our analysis posits this is especially critical for design-intensive markets like home decor and apparel that emphasize localized patterns

Sustainability mechanisms are shifting from cost centers to traceable assets. The take-back recycling (crushing waste for re-spinning) and 100% recycled cotton printing mentioned in the forum [1], paired with disclosure requirements for digital product passports [1], mean that 'where this fabric comes from, what ink was used, and how much waste was produced' will gradually become verifiable data. Our analysis suggests that digital printing holds an inherent advantage in this chain: because it is driven by digital files from the start, recording the materials and energy consumption of each order is far easier than with analog methods, making it easier to interface with future passport-style disclosure requirements

What needs to be balanced is that the forum's description of stalled reshoring and the impact of geopolitical factors, tariffs, and energy costs [1] serves as a reminder that this optimistic mechanism is not without resistance. Our analysis posits that the capital expenditure for digital equipment, the learning curve for technical labor, and the impact on relationships with existing screen-printing clients are all real frictional costs of transition. An inflection point exists; it does not mean the transformation is without cost

Implications for Taiwan's Design and Printing Industry

This section explains the specific meaning of the aforementioned signals for three types of actors in Taiwan, focusing on what is actionable rather than slogans. For the Taiwanese industry, the most direct signal is: the old logic of using screen printing to amortize costs is being eroded from the bottom up by the 500-unit threshold [1]

For small and medium-sized printing plants, we suggest starting with an audit of order structures. The specific approach is to tabulate the past year's orders by batch size (for internal analysis, not for external disclosure) and calculate the percentage of revenue falling under 500 units; if this share is significant and showing an upward trend, digital printing should be advanced from 'consideration' to 'pilot.' The pilot stage should focus on specific categories (e.g., promotional items or small-batch home decor) with single machines, and prioritize the use of water-based pigment inks that pass environmental certification to meet brand compliance demands [1]. For pretreatment, plants can evaluate negotiating mill-level direct shipping with upstream fabric mills to reduce the capital pressure of building in-house wet processes [1]

For designers, the implication is that creative workflows can be rearranged. As proofing cycles shorten [1], designers should proactively incorporate 'parallel multi-version color testing' into proposal standards, leveraging the near-zero marginal cost of modification to explore more colorways and patterns, rather than continuing the conservative habit of 'finalizing the design once' from the screen-printing era. This is also an opportunity for differentiation: localized, limited-edition, and customized patterns, demands that are difficult to economize with screen printing, are the sweet spot for the digital route

For brand owners, the signal concerns supply chain resilience and proactive layout for compliance. The forum's judgment on the return of sustainability regulations and digital product passports [1] means brands should proactively require suppliers to possess traceability capabilities for materials and energy consumption. In practice, brands can include 'capability to support small-batch digital printing' and 'ability to provide production waste recycling solutions' in their vendor selection criteria [1], shifting sustainability from ex-post reporting to ex-ante selection. Our analysis concludes that for Taiwanese brands targeting the EU market, the time value of this proactive layout is higher than simple price comparison of equipment

The common implication across layers is that the window of time is narrowing. Our analysis suggests that as competitors cross the 500-unit cost intersection point, the early movers secure not just equipment, but a lock-in relationship with the brand side regarding compliance and flexibility; once established, such relationships are sticky. The cost of delaying the decision will gradually manifest in the form of 'being excluded from on-demand supplier lists.'

Conclusion and Limitations

This article returns to the research question from the introduction: Has digital textile printing reached an inflection point worthy of production capacity reallocation for Taiwanese printing plants? Synthesizing the three criteria revealed by the FESPA 2026 forum (equipment growth exceeding 15% for three consecutive years, water-based pigment inks passing most EU certifications, and screen printing losing price advantage under 500 units), this article concludes that the inflection point has essentially arrived within mainstream order scales, and its driving force stems from demand fragmentation and regulated sustainability, rather than purely technological push [1]

The core recommendation for the Taiwanese industry is to update the definition of competitive advantage from 'scale-based cost amortization' to 'flexibility and traceability,' and to conduct staged pilots based on order structure rather than a full-scale equipment overhaul

This article must honestly disclose three limitations. First is the single source. The core evidence primarily comes from a single exhibition forum, and the exhibition organizer itself is a stakeholder in the equipment ecosystem; its data should be viewed as internal industry signals rather than neutral statistics, this is also a self-reminder from the critical evaluation of literature using media sources [5][6][2]. Second is the boundary of regional extrapolation. The forum context is based on EU regulations and markets; Taiwan faces different tariff, energy, and supply chain conditions, so the specific figure for the 500-unit threshold may fluctuate locally and must be calibrated against actual cost curves at individual plants. Third is the time slice. This article captures a cross-section of mid-2026; the scope of ink compliance and equipment growth rates may change with subsequent economic and regulatory adjustments

Future research directions include: first, collecting batch-specific cost data from local Taiwanese printing plants to empirically calibrate local intersection points for screen vs. digital costs; second, tracking the actual compliance costs and timeline impacts on Taiwan's export-oriented supply chain once digital product passports are implemented in the EU

Key Takeaways

Digital textile printing equipment has grown by over 15% for three consecutive years, indicating structural rather than cyclical demand [1]

Screen printing has lost its price advantage for runs under 500 units; the inflection point has encroached on mainstream order scales [1]

Water-based pigment inks pass most EU certifications, removing two obstacles: compliance and post-processing [1]

Taiwanese firms should first audit the share of orders under 500 units before deciding on digital pilot timelines, rather than conducting a full-scale equipment overhaul

Evidence comes from a single exhibition forum and should be viewed as an industry signal rather than a neutral statistic, requiring local calibration [1][5]

Extended Thinking

For print manufacturing, the true meaning of the inflection point is the inability to amortize fixed costs; therefore, transformation strategy should start with 'order structure' rather than 'technological novelty,' conducting pilot tests by category and negotiating direct shipping of pretreatment with upstream mills to lower implicit barriers [1]. For design, the near-zero marginal cost of modification makes parallel multi-version testing the new standard, and localization/limited customization is the sweet spot for the digital route [1]. The next step for AI integration lies in pattern making and automated proofing, which can further compress feedback loops; however, the material here has limited focus on its commercial maturity, which is an issue yet to be solved. For SaaS, the biggest opportunity lies in bridging the traceability of materials and energy consumption for digital product passports, turning the file-based advantage inherently present in digital printing into a verifiable compliance asset for brands [1]

References

[2] Hackley C. (2026). Book Review: Market-oriented disinformation research: Digital advertising, disinformation and fake news on social media Diaz RuizC. (2025). Market-Oriented Disinformation Research: Digital Advertising, Disinformation and Fake News on Social Media (1st ed.) London: Routledge. https://doi.org/10.4324/9781003506676. Marketing Theory. DOI: 10.1177/14705931261452313

[3] SMITH P. (1987). A digital optical switch. Optics News. DOI: 10.1364/on.13.12.000033

[4] A Tiny Switch to Make Wheat Cope With Heat. News Digital Object Group. DOI: 10.1111/tpj.0090012

[5] White L., Heap J. (2025). Summarizing Critically Evaluating Digital News and Media Sources. Critically Evaluating Digital News and Media Sources. DOI: 10.4135/9798348845995

[6] White L., Heap J. (2025). Critically Evaluating Digital News and Media Sources Capstone Project. Critically Evaluating Digital News and Media Sources. DOI: 10.4135/9798348846008

FAQ

- Is digital textile printing really cheaper than screen printing now?

- For batches under 500 units, traditional screen printing has clearly lost its price advantage because it relies on quantity to amortize plate-making costs, while digital printing has almost no plate-making costs [1]. However, the actual intersection point fluctuates with each firm's cost structure and must be calibrated using your own data

- Are the equipment growth figures mentioned at FESPA 2026 credible?

- The forum revealed that equipment sales have grown by over 15% for three consecutive years; double-digit growth sustained over three years is better at excluding short-term fluctuations [1]. However, FESPA is an industry exhibition body, so it is advisable to view this as an industry-internal signal rather than neutral statistics [5]

- Should Taiwanese printing plants replace their screen printing equipment now?

- We do not recommend a full-scale replacement. It is advisable to first audit the revenue share of orders under 500 units from the past year. If the share is significant and rising, proceed with single-machine pilots to enter specific categories [1]

- Why are water-based pigment inks important?

- Water-based pigment inks can now pass most EU environmental certifications, effectively removing both compliance thresholds and some post-processing wet stages, further lowering the unit cost of the digital route in high-energy-cost environments [1]

- How will sustainability regulations impact Taiwan's textile printing supply chain?

- The forum assessed that sustainability will return with stronger regulations, with digital product passports requiring disclosure of material usage and environmental footprints [1]. Because digital printing is highly file-driven, it is easier to interface with such traceability requirements, and brand owners should proactively require suppliers to possess this capability

References

- 數位紡織印刷的拐點已到:FESPA 2026 帶給台灣成衣與軟裝印刷廠的訊號 · fespa.com

- Book Review: Market-oriented disinformation research: Digital advertising, disinformation and fake news on social media · doi.org

- A digital optical switch · doi.org

- A Tiny Switch to Make Wheat Cope With Heat · doi.org

- Summarizing Critically Evaluating Digital News and Media Sources · doi.org

- Critically Evaluating Digital News and Media Sources Capstone Project · doi.org

Related articles

The Print × AI weekly

The print and AI know-how designers, brands and enterprises can use before they commit — one email, every week

MINDS Free Tools

Spine width and imposition calculators — skip the manual math, free in your browser.

MINDS Group

Need actual printing or gifting services?

From premium printing to online ordering and festive gifts — the MINDS Group sister brands take it from here.